I.Current Situation of China's Rare Earth Industry

Rare earths are a group of 17 chemical elements in the periodic table of the elements, i.e.,Lanthanum (La), Cerium (Ce), Praseodymium (Pr), Neodymium (Nd), Promethium (Pm),Samarium (Sm), Europium (Eu), Gadolinium (Gd), Terbium (Tb), Dysprosium (Dy), Holmium(Ho), Erbium (Er), Thulium (Tm), Ytterbium (Yb) and Lutecium (Lu), and their congenersScandium (Sc) and Yttrium (Y). According to their atomic weights and physicochemicalproperties, they are divided into light, middle and heavy rare earth elements. The first fiveabove-mentioned elements are light ones, and the rest are either middle or heavy ones.Because of their unique physicochemical properties, rare earth elements are consideredindispensable in modern industry as they are extensively used in areas such as new energy,new materials, energy conservation and environmental protection, aeronautics andastronautics and electronic information, to name but a few.

China is relatively abundant in rare earth resources, and its rare earth reserves account forapproximately 23 percent of the world's total. China's rare earth resources display the followingcharacteristics:

- Their distribution presents a "light north, heavy south" pattern. Light rare earth mines aremainly located in Baotou of the Inner Mongolia Autonomous Region, and other northern areas,as well as in Liangshan of Sichuan province, while ion-absorbed-type middle and heavy rareearth deposits are mainly found in Ganzhou of Jiangxi province, Longyan of Fujian province,and some other southern areas.

- The types of rare earth resources are rather diversified. China has a rich variety of rare earthminerals, including bastnaesite, monazite, ion-absorption minerals, xenotime, fergusonite, andothers, with a relatively complete range of rare earth elements. Among them, the ion-absorptionmiddle and heavy rare earth deposits occupy an important position in the world.

- The associated radioactive elements of light rare earth minerals pose major problems for theenvironment. Most of China's light rare earth deposits ores can be industrially mined, butthorium (Th) and other radioactive elements are difficult to treat, and therefore great attentionmust be paid to its impact on people's health and the ecology when they are mined, smeltedand separated.

- Ion-absorption middle and heavy rare earth ores have poor occurrence conditions. In ion-absorbed-type rare earth deposits, the rare earth elements are absorbed in the soil in the formof ions, making it difficult for industrial exploitation due to sparse distribution and lowabundance rate.

Since the introduction of the reform and opening-up policies in the late 1970s, China's rareearth industry has seen rapid development. Major progress has been made in the researchand development of relevant mining, smelting and utilizing technologies, and the increasingexpansion of the industrial scale has basically satisfied the needs of the nation's economicgrowth and social development.

- A complete industrial system has been achieved. China has developed three major rare earthproduction areas, i.e., the light rare earth production areas in Baotou of Inner Mongolia andLiangshan of Sichuan, and middle and heavy rare earth production areas in the five southernprovinces centering around Ganzhou of Jiangxi province. With a complete industrial systemarmed with mining, dressing, smelting and separating technologies and incorporatingequipment manufacturing, material processing and end-product utilization, China can produceover 400 varieties of rare earth products in more than 1,000 specifications. In 2011, Chinaproduced 96,900 tonnes of rare earth smelting separation products, accounting for more than90 percent of the world's total output.

- The market environment is gradually improving as China is constantly expediting reform in therare earth industry, promoting the development of a market system featuring diversifiedinvestment, independent decision-making by businesses and pricing according to supply anddemand. In recent years, investment in China's rare earth industry has experienced rapidgrowth, the market has been constantly expanded, state-owned, privately owned and foreign-invested sectors coexist, and the value of the rare earth metal market is approaching 100billion yuan. The market order in this sector is gradually improving, and progressivedevelopment is being made in the merger and reorganization of businesses. The old picture ofa "small, scattered, and disorderly" rare earth industry has vanished.

- Scientific and technological level has improved further. After many years of development,China has established a relatively complete R&D system, pioneered numerous technologies ofinternational advanced levels in rare earth mining and dressing, smelting, separating, etc., andits unique mining and dressing processes and advanced separating techniques have laid asolid foundation for efficient exploitation and utilization of rare earth resources. The rare earthnew materials industry has experienced steady development, and industrialization has beenachieved in using rare earths to produce permanent-magnet, luminescent, hydrogen-storage,and catalytic materials, and other new materials, providing support for the restructuring andupgrading of traditional industries, and the development of emerging industries of strategicimportance.

The rapid development of China's rare earth industry has not only satisfied domestic demandfor economic and social development, but also made important contributions to the world's rareearth supply. For many years, China has been faithfully fulfilling its pledges upon its accessionto the WTO, honoring the WTO rules, and promoting fair trade in rare earths. Currently, Chinasupplies over 90 percent of the global market rare earth needs with 23 percent of the world'stotal reserves, its output of permanent-magnet, luminescent, hydrogen-storage and polishingmaterials, which use rare earths as raw materials, accounts for more than 70 percent of theworld's total, and China-produced rare earth materials, parts and components, as well as rareearth end products, such as energy-saving lamps, special and small electric motors and NiMHbatteries, satisfied the development needs of high-tech industries of other countries, especiallythose of the developed countries.

Despite its rapid development, China's rare earth industry also faces many problems, for which China has paid a big price. The following are some of the problems:

- Excessive exploitation of rare earth resources. After more than 50 years of excessive mining, China's rare earth reserves have kept declining and the years of guaranteed rare earth supply have been reducing. The decline of rare earth resources in major mining areas is accelerating, as most of the original resources are depleted. In Baotou, only one-third of the original volume of rare earth resources is available in the main mining areas, and the reserve-extraction ratio of ion-absorption rare earth mines in China's southern provinces has declined from 50 two decades ago to the present 15. Most of the southern ion-absorption rare earth deposits are located in remote mountainous areas. There are so many mines scattering over a large area that it is difficult and costly to monitor their operation. As a result, illegal mining has severely depleted local resources, and mines rich in reserves and easy to exploit are favored over the others, resulting in a low recovery rate of the rare earth resources. Less that 50 percent of such resources are recovered in ion-absorption rare earth mines in southern China, and only ten percent of the Baotou reserves are dressed and utilized.

- Severe damage to the ecological environment. Outdated production processes and techniques in the mining, dressing, smelting and separating of rare earth ores have severely damaged surface vegetation, caused soil erosion, pollution, and acidification, and reduced or even eliminated food crop output. In the past, the outmoded tank leaching and heap leaching techniques were employed at ion-absorption middle and heavy rare earth mines, creating 2,000 tonnes of tailings for the production of every tonne of REO (rare earth oxide). Although more advanced in-situ leaching method has been widely adopted, large quantities of ammonium nitrogen, heavy metal and other pollutants are being produced, resulting in the destruction of vegetation and severe pollution of surface water, ground water and farmland. Light rare earth mines usually contain many associated metals, and large quantities of toxic and hazardous gases, waste water with high concentration of ammonium nitrogen and radioactive residues are generated during the processes of smelting and separating. In some places, the excessive rare earth mining has resulted in landslides, clogged rivers, environmental pollution emergencies, and even major accidents and disasters, causing great damage to people's safety and health, and the ecological environment. At the same time, the restoration and improvement of the environment has also heavily burdened some rare earth production areas.

- Irrational industrial structure. China's rare earth industry has huge over-capacity in smelting and separating. On the other hand, the research and development of rare earth materials and components is lagging behind, its level of rare earth new materials development and end-product application technologies is significantly lower than the advanced international level, and the IPR ownership, and the production and processing technologies of new-type rare earth materials and components are relatively small in number. As a result, low-end products overflow while high-end products are in short supply. China's rare earth metals industry, relatively small in scale, features a low concentration rate with numerous businesses, but lacks large enterprises with core competitiveness. Self-discipline in the industry is also weak, and vicious competition exists to some extent.

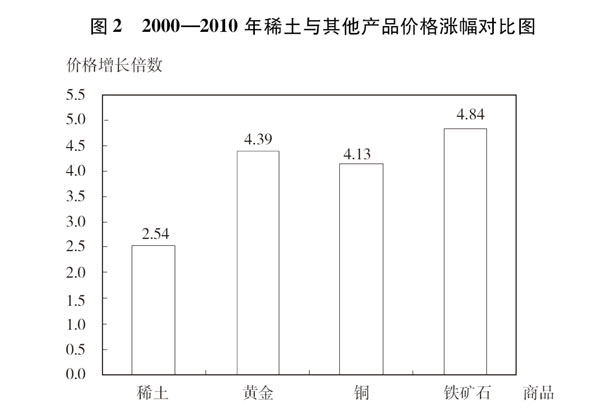

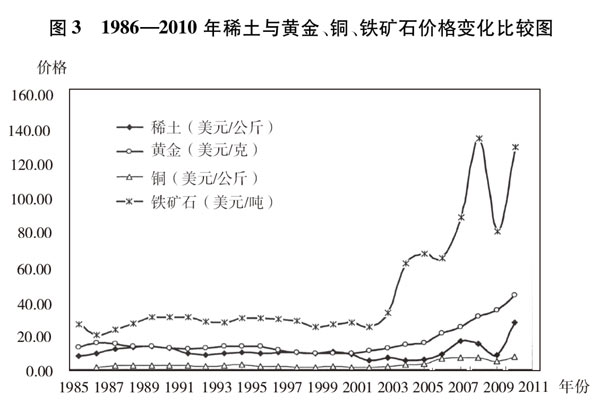

- Severe divergence between price and value. Over quite a long period of time, the price of rare earth products has remained low and failed to reflect their value, the scarcity of the resources has not been appropriately represented, and the damage to the ecological environment has not been properly compensated for. Since the second half of 2010, despite the gradual rise in the price of rare earth products, the rise has been much lower than that in the price rise of other raw materials like gold, copper and iron ore. From 2000 to 2010, the price of rare earth products rose by 2.5-fold, while that of gold, copper and iron ore increased by 4.4-, 4.1-, and 4.8-fold during the same period, respectively.

- Grave smuggling. Due to multiple factors, including domestic and international demand, thesmuggling of rare earth products to overseas markets continues to be a problem in spite of theefforts made by China's customs listing it as a key criminal act to crack down on. From 2006 to2008, the volumes of rare earth products imported from China, according to statistics collectedby from foreign customs, were 35 percent, 59 percent and 36 percent higher than the volumesexported, as statistics released by the Chinese customs show, and the figure from foreigncustoms is 1.2-fold over the Chinese figure in 2011.

To address the salient problems in the development of China's rare earth industry, the Chinesegovernment has tightened supervision over it. In May 2011, the State Council issuedGuidelines on Promoting the Sustainable and Healthy Development of the Rare Earth Industry(hereinafter referred to as the "Guidelines"), attaching more importance to the protection ofresources and the environment, and the realization of sustainable development. According tothe "Guidelines," the government - in accordance with law - will strengthen control over themining, production, circulation, import and export, and other links of the rare earth industry, andstudy and formulate as well as amend and improve related laws and regulations on theadministration of this industry. The Chinese government has established an inter-departmentalcoordinating mechanism for the rare earth industry to make overall plans and study of thenational strategy, program, plan, policy, and other important issues concerning thedevelopment of the rare earth industry. The state has also set up a rare earth office tocoordinate and propose plans on the mining, production, reserve, and import and export ofrare earth materials. The relevant departments of the State Council will perform their respectiveadministrative functions accordingly. In April 2012, Association of China Rare Earth Industrywas founded with official approval. It is expected to play an important role in promoting self-discipline in the industry, regulating the industrial order, and proactively carrying outinternational cooperation and exchanges, among other functions. A year or so has passedsince the implementation of the "Guidelines," the transformation of the development pattern ofChina's rare earth industry has picked up speed, and significant improvement has been seen inits development order.