Clarity required on RMB internationalization

- By John Ross

0 Comment(s)

0 Comment(s) Print

Print E-mail China.org.cn, October 27, 2015

E-mail China.org.cn, October 27, 2015

|

|

|

The RMB's trade based internationalization benefits China but premature attempts to rival the dollar would be harmful, the writer of this article argues. |

Two apparently contradictory trends in RMB internationalization emerged recently. Positively, the RMB overtook the Yen to become the fourth most used currency for international payments; unfortunately, some negative trends appeared in China's position in the international economy.

China's foreign exchange reserves fell almost $500 billion, from slightly under $4 trillion in June 2014 to $3.5 trillion in August 2015. This is seen as evidence of exit of capital from China unconnected with fruitful overseas investment. A small 2 percent RMB devaluation in August was followed by further losses to China's foreign exchange reserves in an attempt to stabilize the currency.

However, both trends really reflect fundamental features of China and the international economy. Examining other countries experience and economic theory explains the processes involved.

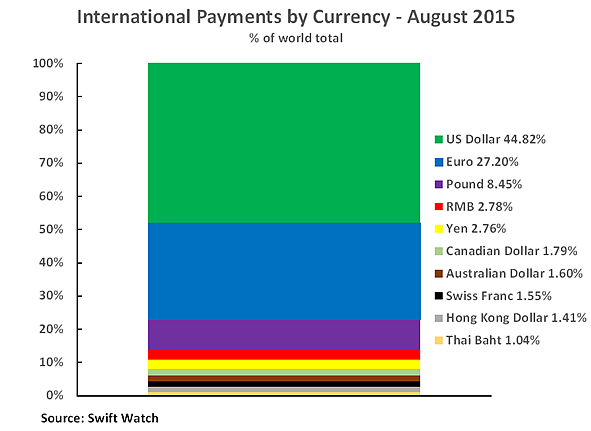

Figure 1 shows the RMB's place in global payments. The dollar's dominance and RMB's peripheral position is clear. The dollar accounts for 44.82 percent of international payments. The dollar dominance is still more striking if it is understood that the Euro's 27.20 percent primarily reflects payments within the Eurozone; without these the global dominance of the dollar is still clearer.

Global payments in dollars are 16 times greater than the RMB (2.78 percent). Payments in combined dollars and Euros are 25 times greater than those in RMB. Hence, talk of the RMB being "in fourth place" in international payments behind the dollar, without stating the gap between the two, may be correct but is misleading if the scale of this gap is not also made clear.

This gap becomes clearer if it is understood that the RMB is primarily used internationally in relation to China's trade - functioning as a useful "hedge" against currency fluctuations. By April 2015, 31 percent of payments between China (including Hong Kong) and the Asia-Pacific region were in RMB. Such trade operations make limited foreign accumulation of RMB necessary, and are a soundly based development reflecting China's position as the world's largest goods-trading nation.

However, aside from this useful function, the RMB's role in international payments is still peripheral and for fundamental reasons cannot be expanded rapidly. For example by the end of 2014, 63 percent of all countries foreign exchange reserves were in dollars, 22 percent in Euros, and 1 percent in RMB.

It is sometimes argued that the RMB's international role could grow rapidly if, for example, later this year the IMF includes the RMB in its currency basket for its Special Drawing Rights (SDRs).

However, this argument confuses reserves for current trade transactions and capital holdings of which foreign exchange reserves are a part. Certainly, the RMB should be included in the basket of currencies in SDRs due to China's weight in the world economy. But this will not change the fundamental situation. SDRs are neither a currency nor a claim on IMF funds - only a claim on IMF member's currencies. SDRs can essentially only be part of countries foreign exchange reserves, constituting less than 3 percent of these. In practical terms, SDRs are essentially only an accounting unit with little role in actual transactions.

Go to Forum >>0 Comment(s)